Tanker Shipping: Is the Oil Market Rebalancing or Not?

© Igor Yu. Groshev / Adobe Stock

© Igor Yu. Groshev / Adobe Stock

Demand

The one key factor to watch is the one thing that’s impossible to measure accurately on a global scale, oil stocks.

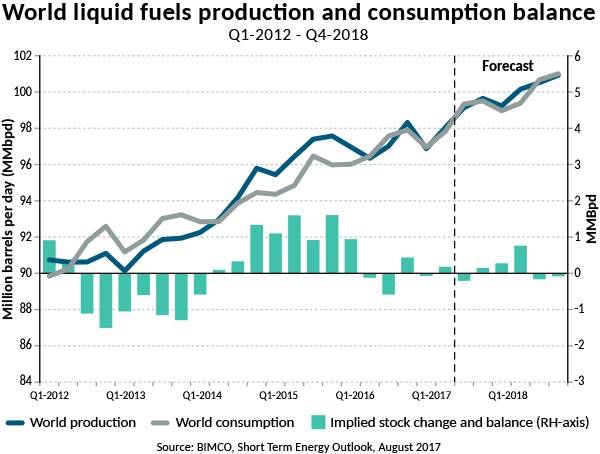

Global stocks for both crude oil and oil products rose significantly following the sharp fall in crude oil prices in the second half of 2014. But while this may seem to be in the past, it is still haunting the oil market and the oil tanker market. Demand in the tanker market is below normal levels and will only increase once the global oil stocks have been reduced.

Tanker shipping enjoyed above-normal demand as the stocks were building, but will continue to suffer as long as they remain high. The strong fleet growth in 2016 and 2017 only makes the downturn tougher on owners and operators struggling with stretched balance sheets, as earnings drop.

So, what is the right level of future oil stocks? It’s anyone’s guess now, but BIMCO believes that it is much lower than the estimates of the ‘money managers and bull traders’, but not as low as the level seen before the rise in 2014.

Global oil demand has grown markedly since then, and it seems fair to strive toward a level equal to a given number of days of supply, rather than a multiannual absolute average.

BIMCO believes that some rebalancing has taken place over recent months, but much more is needed. Data regarding OECD-stocks only provides an indication of how the market is developing in one part of the world. Likewise, any draw down on stocks in the US should not be used as a global proxy, as the U.S. only holds 1/6 of OECD stocks.

Bearing in mind that if global stocks have a surplus of 180 million barrels, it will take one whole year to reduce that at the rate of 500,000 barrels per day (bpd). The Energy Information Administration (EIA) has estimated that global liquid fuel stocks have risen by more than 1m bpd on average for six quarters in a row, that’s at least 540 million barrels of stock stored.

Seaborne trade

The global tanker industry is directly linked to the global oil industry. Right now, demand for seaborne transport of oil is below normal and fleet growth is high, which means that the fundamental balance is uneven. The result is declining tanker earnings with the main culprit being the fast-growing fleet.

We tend to forget however, that demand is not that bad. Looking beyond the regular draw on stocks, other demand factors remain strong. US gross input to petroleum refineries hit an all-time high in the week ending May 26, when 17.7 million bpd were refined. Global oil demand as forecasted by International Energy Agency (IEA) may pass the 100 million bpd mark for the first time, hitting 100.1 million bpd in Q4-2018, and for 2017, growth has been revised up to 1.5 million bpd. In addition, China is still believed to be increasing its strategic petroleum reserves (SPR) and crude oil imports were up by 13.8 percent year-on-year in the first half of 2017 hitting 8.55 million bdp on average.

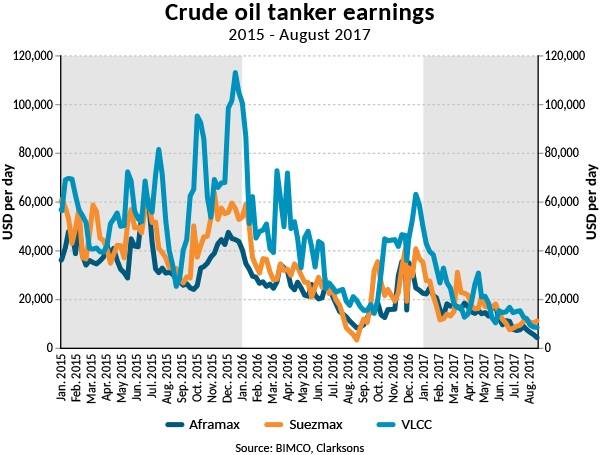

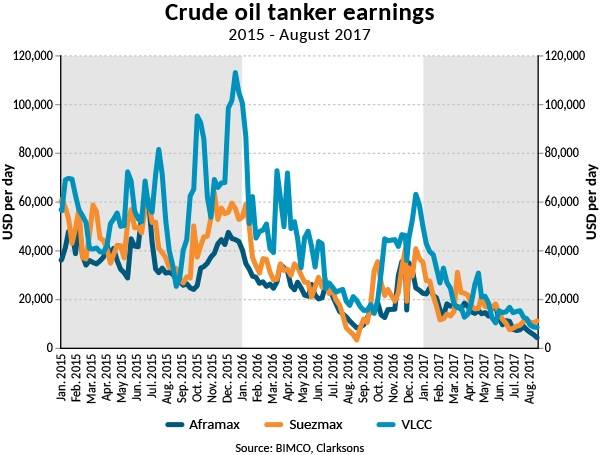

Earnings for VLCCs in the spot market are as low as $8,775 per day, a level last seen during the difficult years of 2011-2013. The year-to-date average stands at $20,489 per day. Based on a set of assumptions, BIMCO estimates that spot trading VLCCs built in 2005 and later are loss making at that level, because of heavy financing costs. For the whole industry, any profits made from older ships do not outweigh the losses of the younger vessels.

As earnings very often follow from one segment to the next, suezmax and aframax ships are suffering too.

Earnings for the oil product tanker sector on average appears to have stopped falling, as they dropped steadily throughout 2016, reaching the present level at the end of the year. BIMCO is forecasting that average earnings in this segment will also be loss-making.

MRs have made no more than $10,040 per day, while Handysize have dropped to $7,658 in 2017 down from $8,962 in 2016. LR1s have a year-to-date average of $7,873 and LR2 $9,235 per day.

Supply

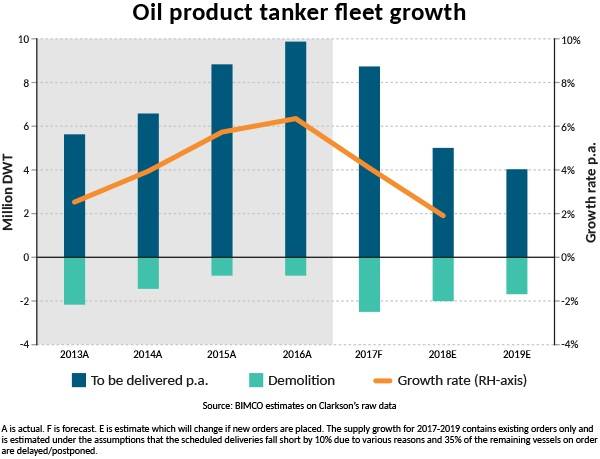

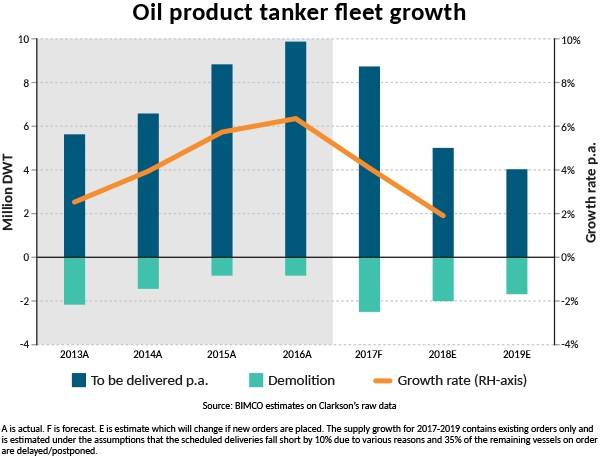

The tanker fleet is growing strongly. By mid-August, the crude oil tanker fleet had grown 4.3 percent year-to-date, and the oil product tanker fleet had grown by 3.6 percent.

Deliveries into the crude oil tanker fleet, include 36 VLCC, 41 suezmax and 23 aframax plus some panamax and smaller units. The crude oil tanker fleet expansion remains on course for a six-year-high, measured in DWT, however, the fleet growth percentage is down from last years’ 5.9 percent, to 4.7 percent for the full year of 2017.

Meanwhile, 23 LR2, equal to 45 percent of the total added oil product tanker capacity overshadowed the recent years’ favorite: MR, as ‘only’ 38 new ships were delivered during the first seven and a half months.

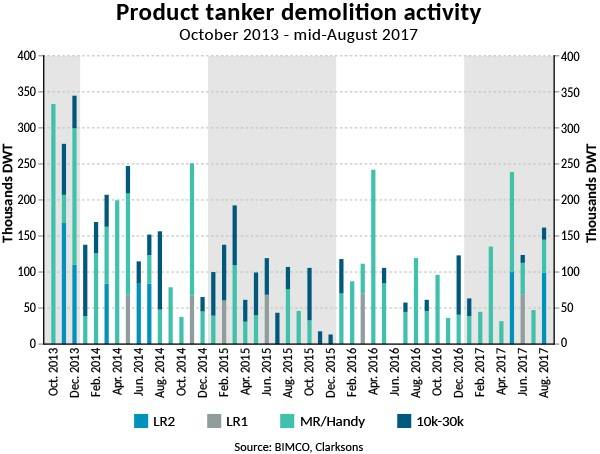

The fast-growing fleets come as no surprise. But the continued low levels of demolition in both tanker segments are a roadblock to changes to the current poor earnings environment in the freight market and a possible recovery.

The fact that one VLCC was reportedly sold for demolition in April, but was then subsequently sold to a new owner, one month later at a higher price, seems irrational as overcapacity is increasing among crude oil tankers in general and VLCCs in particular.

Among oil product tankers, just two LR2 left the fleet in 2017, a year that has seen MR, almost exclusively being demolished.

BIMCO continues to believe that demolition will pick up during the final five months of 2017, but the actual demolition rate only amounted to one third of forecasted full year levels by mid-August. The ongoing poor freight market conditions will drive demolition.

Over the last four months, shipyards have been busy signing new orders for tankers. Among them were 14 LR2 and 14 suezmax ordered in June, supplementing the nine VLCCs ordered in May. In total 32 VLCCs have now been ordered in 2017, up from 12 in the first quarter.

Assuming 2.5 million DWT of oil product tanker capacity will be demolished; fleet growth will hit 4.1 percent in 2017. Should demolition fall short of that by 1 million DWT, the fleet will expand by 4.8 percent.

Outlook

Not a day goes by without a story about global oil stock levels. Many of them trying to be the messenger of positive news for the oil market and the tanker shipping market. However, sometimes business interests and wishful thinking are not supported by facts. Money managers and financial traders run businesses which are very different from the shipping industry.

As OECD compliance with the extended output cut falls to hit 78 percent in July (IEA), U.S. shale oil production is rising, and Nigeria and Libya have some export potential left. So, oil supply seems to rise alongside oil demand.

On the geopolitical scene, Venezuelan exports to the U.S. amounting to 800,000 bpd for the past four years face a low risk. As Venezuela’s crude oil is very heavy and sour, it has no obvious substitutes, and is compatible to sophisticated refineries in the U.S. Gulf (including some Venezuelan owned). There may be U.S. sanctions aimed at political targets, but we do not expect oil exports to be hit hard.

Following its annual peak in August, the global refinery runs will decline seasonally due to maintenance, by 1.5 million bpd during September and October, before throughput picks up again in November for the winter season.