Lower Oil Price Effect on GCC Economies in 2015

Image: Coface

The Brent oil price per barrel lost more than 50% of its value from $114 in June 2014 to the current price of about $50. Coface expects it to average at $75 on average in 2015. This bearish trend is pressurizing the hydrocarbon sector in major oil producing countries and will have an impact on GCC economies.

The Gulf Cooperation Council (GCC) economies are deeply dependent on the hydrocarbon sector despite their efforts to diversify. The oil industry remains their main source of fiscal revenues and represents more than 80% of fiscal income. A prolonged oil price slump will inevitably affect their economies through a risk of fiscal or current account imbalance. In the longer term, gulf oil exporters risk a decline in their fiscal surpluses over time, especially since they have undertaken large public spending programs coupled with generous energy subsidies.

Not all GCC countries are geared to face an oil price shock. However, some of these countries, Saudi Arabia or Abu Dhabi specifically, have enough foreign exchange reserves to continue public spending and public projects to support their economies. Others like Qatar and Dubai are sufficiently diversified to spread their risk and rely on other sources of income. The more fragile they are to the current oil price collapse may dampen public spending and affect their economies (like Bahrain).

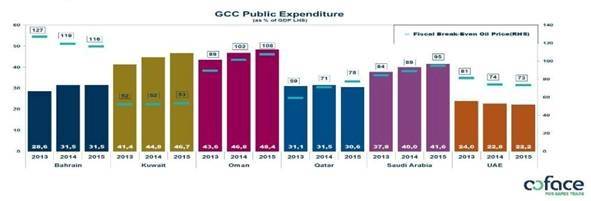

Saudi Arabia remains the largest oil producer in the region and earns the GCC’s largest foreign exchange reserves. It seems to have enough resources to cope with a fall in the oil price. After the Arab spring, Saudi Arabia began a public spending program in response to social tensions. This program induced both domestic and extra budgetary expenditure that raised the break-even oil price (the average price at which the budget of an oil exporting country is balanced) from $70 in 2010 to more than $90 in 2015.

The Saudi authority pledged that its economy would not suffer from a fall in the oil price and that the country would maintain its public support for the non-oil sector. However, it seems likely that without a decrease in public spending, Saudi Arabia is expected to have a public deficit in 2015. Coface’s 2015 GDP forecast for Saudi Arabia is 3.8% and the Coface Country Risk Assessment is A4.

In the Emirates, Coface has witnessed a different scenario. Abu Dhabi owns more than 95% of UAE oil reserves and is able to resist an oil price shock. Abu Dhabi’s substantial foreign assets (the Abu Dhabi Investment Authority fund) and fiscal surplus may provide a buffer against moderate oil price shocks, but a prolonged fall in the oil price would reverse the accumulation of savings and ultimately result in fiscal shocks in the long term.

Dubai continues to expand its role as a hub of finance, retail and wholesale trade, as well as a major tourism and real estate investment destination for the wider region. Due to the diversification of its fiscal revenues, the drop in the oil price will affect the fiscal budget to a lesser extent. Besides, the Emirates may reach a budget surplus in 2014. However, the risk of a destabilization of the Dubai stock market affecting GREs (Government relates entities), due to a prolonged drop in the oil price, remains. Ajman, Fujairah, Ras al-Khaimah, Sharjah and Umm al-Quwain may be affected more severely but they will benefit from the support of Abu Dhabi and Dubai. Coface’s 2015 GDP forecast for Dubai is 4,2% and Coface’s Country Risk Assessment is A3.

Qatar may witness a decrease in its fiscal and external surpluses, slowing QIA (The Qatar Investment Authority) asset accumulation, and weakening financing conditions for Qatar’s large investment program for the 2022 Football World Cup. However, the non-oil sector’s double digit growth will balance the negative effect of the oil price fall. Coface’s Qatar 2015 GDP forecast is 5.2% and Coface’s Country risk Assessments is A3.

Bahrain State’s budget deficit is expected to continue to rise quicker as a consequence of the recent fall in the oil price. With the highest breakeven oil price in the region and its non-oil sector deteriorating, the kingdom will suffer from the oil market decline. This situation may weaken the Bahrain King Family’s power in a climate of wide political instability after the controversial election in November 2014. Coface’s Bahrain GDP forecast for 2015 is 3% and Coface’s Country Risk Assessment is A4.