Effects of Price Slump Vary among Oil Firms -EIA

Figure 1 (Source: EIA)

Figure 1 (Source: EIA)

Figure 2 (Source: EIA)

Figure 2 (Source: EIA)

EIA: 2015 financials reveal significant differences across U.S. onshore-only producers

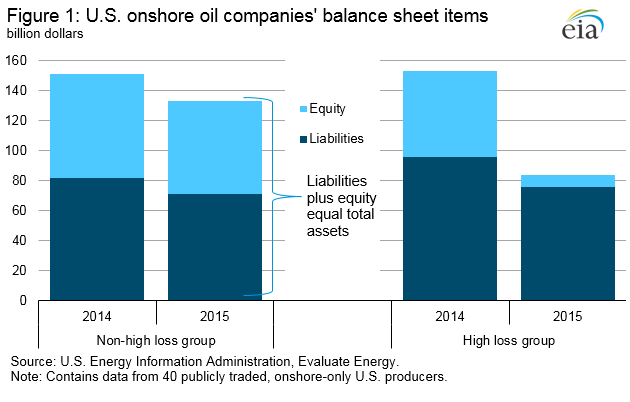

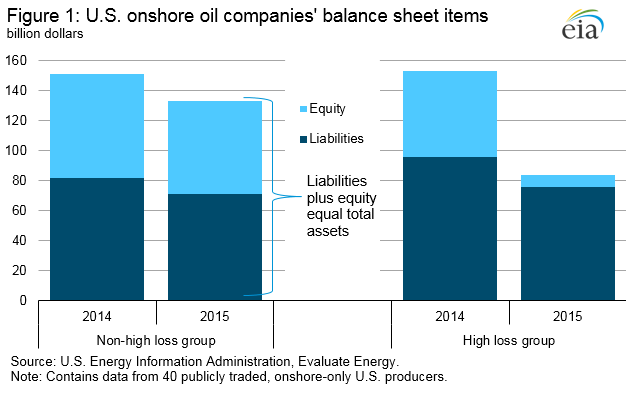

Analysis of the annual reports of 40 publicly traded onshore-only U.S. oil producers reveals combined losses of $67 billion in 2015, driven by significant reductions in sales revenue and write-downs of assets following the decline in crude oil prices over the last 18 months. However, there are significant differences across these companies. Eighteen of these companies, referred to here as the high loss group (HLG), reported 2015 losses in excess of 100 percent of their equity. The HLG companies were more vulnerable to losses in an environment of falling oil prices than companies outside the group because they had more debt and proved reserves with a smaller economic margin between production cost and wellhead value. These same factors may limit the borrowing ability of the HLG companies, which could constrain their drilling and completion activities and thereby limit their production activities under current market conditions.

The aggregate balance sheets for the 18 HLG companies and the 22 non-HLG companies were quite similar at the end of 2014. Each group held roughly half of combined total assets (Figure 1). However, there were some major differences in underlying capital structures across these groups. The HLG companies had $57 billion in long-term debt, and a long-term debt-to-shareholder-equity ratio of 99 percent. In contrast, the non-HLG companies had total long-term debt of $40 billion, 58 percent of the shareholders' equity.

2015 financials reveal significant differences across U.S. onshore-only producers

Analysis of the annual reports of 40 publicly traded onshore-only U.S. oil producers reveals combined losses of $67 billion in 2015, driven by significant reductions in sales revenue and write-downs of assets following the decline in crude oil prices over the last 18 months. However, there are significant differences across these companies. Eighteen of these companies, referred to here as the high loss group (HLG), reported 2015 losses in excess of 100 percent of their equity. The HLG companies were more vulnerable to losses in an environment of falling oil prices than companies outside the group because they had more debt and proved reserves with a smaller economic margin between production cost and wellhead value. These same factors may limit the borrowing ability of the HLG companies, which could constrain their drilling and completion activities and thereby limit their production activities under current market conditions.

The aggregate balance sheets for the 18 HLG companies and the 22 non-HLG companies were quite similar at the end of 2014. Each group held roughly half of combined total assets (Figure 1). However, there were some major differences in underlying capital structures across these groups. The HLG companies had $57 billion in long-term debt, and a long-term debt-to-shareholder-equity ratio of 99 percent. In contrast, the non-HLG companies had total long-term debt of $40 billion, 58 percent of the shareholders' equity.

A high debt-to-equity ratio can present challenges in the face of falling revenue, which most U.S. oil producers experienced in 2015 because of lower oil prices. A company agrees to the terms of a bank loan or bond issuance to fund projects with the expectation that its activities will generate sufficient revenue to service the debt and eventually repay it. Debt on the balance sheet implies future cash outflows. The need to service large amounts of debt as revenues declined made companies with high debt-to-equity ratios more vulnerable to losses than companies with less leverage in their capital structures.

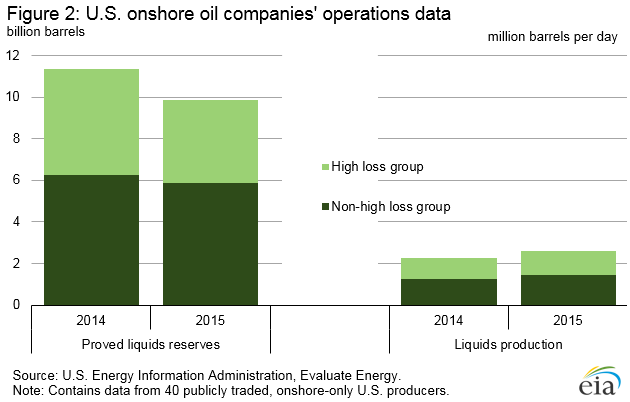

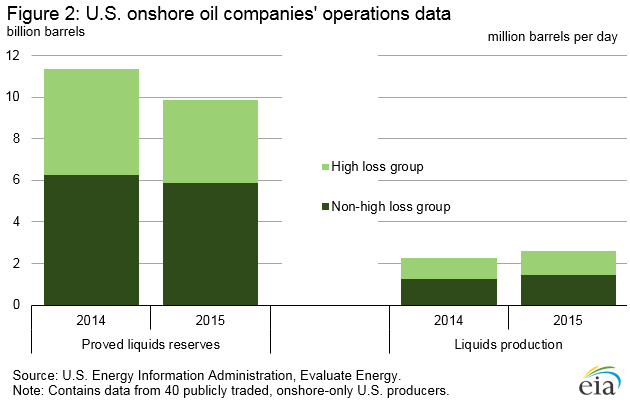

The 18 HLG and 22 non-HLG companies had similar average rates of production in 2015, as the former and latter group collectively produced 1.2 million barrels per day (b/d) and 1.4 million b/d respectively (Figure 2). However, the two groups differed significantly in the extent to which their proved reserves, defined as the estimated quantities of oil and natural gas that analyses of geologic and engineering data demonstrate with reasonable certainty are recoverable under existing economic and operating conditions, declined during 2015. The U.S. Securities and Exchange Commission requires companies to value proved reserves based on the average of crude prices on the first trading day of each month for the year. Using, for example, front month West Texas Intermediate futures closing prices for the first trading day in each month of 2015, this value was $50.13 per barrel, 47 percent below the average for 2014. Proved oil reserves reported by the HLG companies declined by 1.1 billion barrels, a 21 percent reduction from the 2014 level. For companies outside the HLG, proved reserves declined by 374 million barrels, only a 6 percent reduction from their 2014 level. The higher percentage decline in proved reserves for the HLG companies may in part reflect the fact that the reserves they held at the end of 2014 were lower in quality than those of the non-HLG companies, in the sense that they included a higher percentage of volumes with a relatively low margin between their wellhead value and their production cost, making them more sensitive to the recent decline in oil prices.

Reductions in proved reserves are reflected as an impairment charge or a write-down, representing a decrease in the value of the company's assets. Many oil companies that receive regular lines of credit from banks to meet short-term cash needs are subject to borrowing caps that are based on the value of expected cash flows from a company's reserves. Many companies are currently undergoing a redetermination of their credit limits, and those with high leverage or lower quality assets could face significant curtailment of their access to short-term credit that could in turn constrain their drilling and completion operations, with direct implications for their production from new wells in the near term.

U.S. average regular gasoline retail price and diesel fuel prices increase

The U.S. average regular gasoline retail price increased seven cents from the previous week to $2.14 per gallon on April 18, down 35 cents from the same time last year. The Midwest price rose nine cents to $2.06 per gallon. The Rocky Mountain and Gulf Coast prices each increased eight cents per gallon to $2.08 per gallon and $1.91 per gallon, respectively. The East Coast price increased six cents to $2.10 per gallon, followed by the West Coast price, up three cents to $2.59 per gallon.

The U.S. average diesel fuel price increased four cents from the previous week to $2.17 per gallon, down 62 cents from the same time last year. The Gulf Coast price increased five cents to $2.05 per gallon, followed by the West Coast price, up four cents to $2.37 per gallon. The East Coast, Rocky Mountain, and Midwest prices each rose three cents to $2.22 per gallon, $2.17 per gallon, and $2.11 per gallon, respectively.

Propane inventories gain

U.S. propane stocks increased by 1.2 million barrels last week to 68.9 million barrels as of April 15, 2016, 6.9 million barrels (11.1 percent) higher than a year ago. Gulf Coast and Midwest inventories increased by 0.6 million barrels and 0.5 million barrels, respectively, while Rocky Mountain/West Coast and East Coast inventories each rose by 0.1 million barrels. Propylene non-fuel-use inventories represented 5.7 percent of total propane inventories.